The deductibility of advice fees has long been a point of uncertainty – especially when those fees relate to life insurance advice, super structuring, or bundled strategies.

While 2024 saw clearer guidance emerge from the ATO (TD 2024/7), the reality is that most scenarios still require interpretation and professional judgement.

Industry bodies including the FAAA have released practical support materials, but they don’t always go into the right level of detail needed for risk-specific advice. That’s where this article – and a supporting calculator – aim to help. They’re designed specifically for advisers working in the life insurance and superannuation advice space.

During a recent Risk Hub webinar, Ben Martin (Head of Individual Advice Strategy at AIA) offered pragmatic insights into the application of TD 2024/7. He explained that while deductibility can be claimed in various scenarios, it needs to be grounded in the nature of the advice, the strategies involved, and an adviser’s ability to demonstrate a fair and reasonable apportionment. As Ben said in the session:

“It’s not about trying to find an artificial way to claim more, it’s about applying the rules practically and documenting why you’ve done it that way.”

You can check out the full session on Risk Hub, and now that formal guidance is out, the principles discussed there remain helpful context.

Quick Overview

Initial advice fees are generally not deductible unless they directly relate to:

- Income-producing advice (e.g. Income Protection)

- Managing tax affairs (e.g. structuring ownership via super)

- Strategic comparisons with tax outcomes (e.g. super vs non-super ownership)

Ongoing advice fees may also be deductible, particularly where they support the management of tax-effective cover or contribution strategies.

Deductibility under s 8-1 or s 25-5 depends on the nature of the advice and whether the adviser is authorised to provide tax (financial) advice.

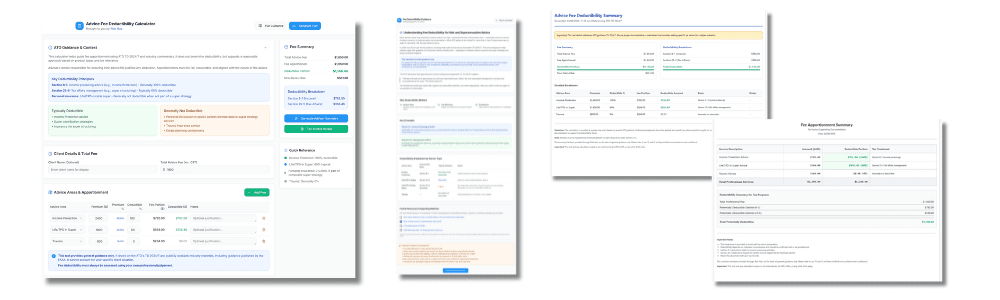

Sample Fee Apportionment Table

The table below shows how a $1,650 advice fee (incl. GST) might be apportioned across a typical recommendation, based on premium weightings:

| Cover Type | Premium | Premium % | Fee Portion | Potential Deductibility | Deduction Basis | Deductible Portion |

| Income Protection | $1,800 | 33% | $540 | 100% | s 8-1 | $540 |

| Life (inside super) | $1,200 | 22% | $360 | 60% | s 25-5 | $216 |

| TPD (inside super) | $1,000 | 18% | $300 | 60% | s 25-5 | $180 |

| Life/TPD (outside super) | $ 500 | 9% | $150 | 0–60%* | Not deductible* | $0.00 (or up to $90) |

| Trauma | $1,000 | 18% | $300 | Generally not deductible | Not deductible | $0.00 |

| Total | $5,500 | 100% | $1,650.00 | $936.00 (to $1,026) |

* A portion of Life/TPD advice outside super may be deductible if it involved meaningful tax structuring considerations (such as weighing up in/out strategies). Strong documentation is essential in these cases.

In many scenarios, the advice has likely focused on structuring ownership and funding across super and non-super environments – with tax, access, and contribution rules forming a key part of the recommendation. The end result may have included a combination of cover (e.g. one policy inside super, the other outside but super-linked). Where this reflects a cohesive strategy, it may be reasonable to apply a similar deductibility approach to the non-super component as was used for the in-super cover (e.g. 60%)

Key Takeaways for Advisers

- Use premium proportions as a reasonable proxy for advice fee apportionment

- Consider deductibility based on the strategy – not just the product type

- Document your rationale and retain a copy for your file or invoice support

- Use available tools, but remember – this isn’t the detail in the tax ruling – it’s practical guidance on it

Looking for a Tool to Help?

A Tax Deductibility Helper (calculator and guide) is now available via Risk Hub. It’s designed to help you:

- Input cover types and premiums

- Apportion your advice fee

- Review the potential deductibility for each part of the strategy

- Generate a simple summary for client files or use in your tax invoice

The calculator is available is aimed at saving time, ensuring consistency, and giving you a helpful record of your approach.

You can explore it here: Resource – Tax Deductibility Helper

Final Word

This guide reflects practical interpretation of ATO TD 2024/7 and guidance developed by the FAAA and other associations. It has also benefited from feedback by adviser-facing specialists like AIA’s Ben Martin. While it doesn’t replace formal tax advice, it’s built with the risk adviser in mind – balancing simplicity with sensible guidance.

Like always, your judgement, documentation, and licensee approval are key.

Disclaimer

This article reflects a simplified interpretation of the ATO’s guidance and current industry best practice. It is not legal, tax, or compliance advice. Please refer to TD 2024/7, FAAA materials, and your licensee guidance, and seek formal advice where appropriate.

Further Reading & Source Materials

These publicly available documents provide deeper context on advice fee deductibility:

📄 FAAA Quick Reference Guide: Tax Deductibility of Financial Advice Fees

📘 Tax Deductibility of Financial Advice Fees: A Practical Guide to Implementation

🧾 ASIC INFO 268: Tax (Financial) Advice Services – Relevant Providers